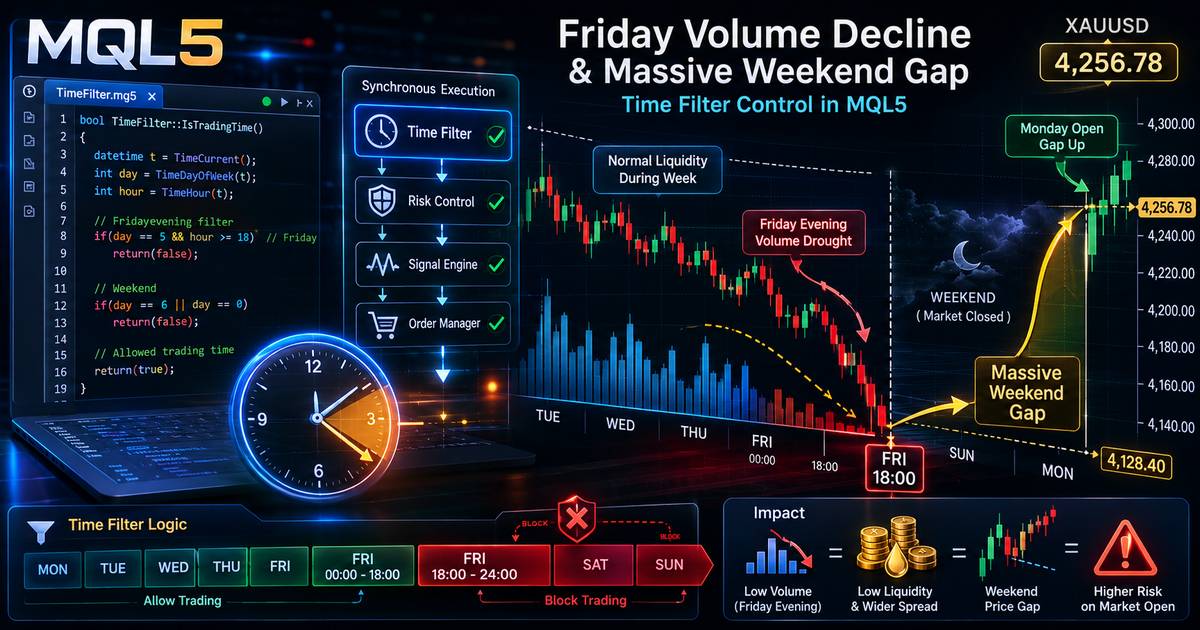

Deploying a high-performance quantitative system involves more than just optimizing mathematical entry indicators. To safeguard account equity, an algorithm must possess situational awareness regarding temporal market states. Friday night operations and weekend market closures present significant architectural challenges for trend-following networks. As institutional capital leaves the market on Friday afternoon, order-book depth collapses, causing spreads to expand aggressively. This guide demonstrates how to program a production-ready, object-oriented MQL5 Time Filter module designed to automatically isolate your trade execution engine from these high-risk periods.

The Systemic Threat: Friday Low Liquidity and Weekend Gaps

Retail participants frequently make the mistake of running their execution loops continuously, assuming that price movement behaves uniformly across all 24 hours of a trading day. In reality, the market structure changes dramatically during transition windows. As the New York session closes on Friday, interbank liquidity networks scale back their automated market-making algorithms.

Executing new orders during this period forces your system to absorb toxic slippage. Furthermore, holding unhedged directional exposure across a weekend leaves your capital completely vulnerable to macroeconomic weekend gaps that can easily bypass hard stop losses, resulting in catastrophic margin stress. To understand how unmitigated structural leverage compounds risk during extreme market shifts, read our detailed analysis on the mathematics of leverage collapse in retail trading portfolios.

MQL5 Core Architecture: Navigating MqlDateTime Structures

To create a scalable time calculation engine, we bypass simple string comparisons, which are computationally inefficient and prone to failures. Instead, we leverage the native MQL5 MqlDateTime structure. This native object allows the application thread to decompose timestamp integers into manageable properties like day of the week, hours, and minutes instantaneously.

Crucially, institutional filters must always track TimeCurrent() (Broker Server Time) rather than TimeLocal() (the clock of your localized VPS or machine). This ensures that no matter where your system is globally deployed, its operational parameters stay synchronized with the actual asset contract data.

Practical Implementation: Production-Grade Time Filter Engine

To seamlessly complement our foundational multi-timeframe trend architecture outlined in Building a Trend-Following Algorithm: Multi-Timeframe EMA Filters in MQL5, your trade execution block must check temporal restrictions before firing any order.

The production-ready, object-insulated logic below provides an elite safeguard block that restricts new positions after Friday 18:00 Server Time and keeps them blocked through the weekend:

//+------------------------------------------------------------------+

//| Validates Market Operational Safety Boundaries |

//| Returns true if conditions are safe for executing new trades |

//+------------------------------------------------------------------+

bool IsTimeSafeToTrade()

{

MqlDateTime currentDateTime;

// Synchronize structural object variables with current broker server clock

if(!TimeCurrent(currentDateTime))

{

Print("Critical Warning: Failed to retrieve historical server time metrics.");

return false; // Fail-safe fallback to prevent trading during initialization drops

}

// 1. Isolate and eliminate weekend execution requests (Saturday = 6, Sunday = 0)

if(currentDateTime.day_of_week == 0 || currentDateTime.day_of_week == 6)

{

return false;

}

// 2. Enforce Friday evening suspension rule (Aborting new setups after 18:00 Server Time)

if(currentDateTime.day_of_week == 5) // Friday

{

if(currentDateTime.hour >= 18)

{

return false; // Restrict order routing during high-spread rollover horizons

}

}

return true; // The system resides completely within normal operational parameters

}

By wrapping this filter logic into your main execution routine—such as if(IsTimeSafeToTrade() && IsTrendAligned())—the Expert Advisor completely isolates its order routing engine from high-risk periods, ensuring its trend-following edge functions only when structural institutional volume is present.

Algorithmic Optimization and VPS Synchronization Factors

- Intraday Spread Verification: In addition to checking structural clock parameters, systems should verify live transaction realities by querying

SymbolInfoInteger(_Symbol, SYMBOL_SPREAD). If late-session spreads exceed your historical boundaries, the trade should be immediately aborted. - Handling Global Clock Variations: Different brokerage firms run on varying server clock matrices (typically GMT+2 or GMT+3 to line up with New York daily bar boundaries). Ensure your hardcoded hour limits (e.g., 18:00) match your specific broker's data feed configuration.

- Automated Emergency Liquidation: For high-leverage portfolios, developers often adapt this time engine to not only block *new* entry placements on Friday night, but to dynamically close out any floating intraday trade files to eliminate weekend overnight risk entirely.

Temporal Risk Architecture Parameters

Review our architectural index defining how systematic execution matrices shift across different temporal profiles:

| Temporal Profile State | Core Architecture Behavior | Systemic Risk Mitigation | Execution Priority |

|---|---|---|---|

| Mon 02:00 - Fri 17:59 | Standard Operational Loop Active | Normal statistical variances managed by filters | Full Execution Rights |

| Friday 18:00 - 23:59 | Time Filter Intercept Engaged | Eliminates toxic spreads & pre-weekend adjustments | ABORT New Executions |

| Sat 00:00 - Sun 23:59 | System Sleep Mode Enforced | Insulates balance from weekend gaps & news spikes | SHUTDOWN Core Engine |

Conclusion: Strategic Capital Preservation

Developing a long-term profitable trend algorithm requires focusing on when *not* to trade just as much as optimizing your entry indicators. Implementing a native MQL5 time safety block shields your capital curves from structural changes in liquidity, protecting your portfolio from the extreme drawdowns that frequently catch uncalibrated trading algorithms off guard.

Quantitative Development FAQ

Why should automated systems completely abort new executions on Friday afternoons?

During late Friday sessions, institutional trading desks liquidate intraday blocks, resulting in an abrupt evaporation of market liquidity. Operating during these hours exposes Expert Advisors to excessive spread widening, toxic slippage, and catastrophic weekend gap risks.

What is the difference between TimeCurrent() and TimeLocal() when designing filters in MQL5?

TimeCurrent() returns the last known server time of the broker, which dictates contract expirations and chart history alignment. TimeLocal() returns the local clock of the machine running the terminal (PC or VPS). For multi-broker compatibility, institutional logic should always depend strictly on TimeCurrent().