Architecting an institutional-grade Expert Advisor (EA) in MetaTrader 5 demands perfect interaction with structural market parameters. In quantitative logic, static stop losses and random entry boundaries represent programmatic vulnerabilities. To insulate capital from volatile liquidations, an automated execution engine must locate real-time market structure boundaries (Swing Highs and Swing Lows). MQL5 equips algorithmic developers with native iHighest and iLowest functions to parse historical data arrays efficiently. Understanding how to deploy these memory-optimized functions is critical to transforming volatile retail code into a robust, high-performance automated system.

The Architectural Paradigm: Memory Offsets vs. Price Arrays

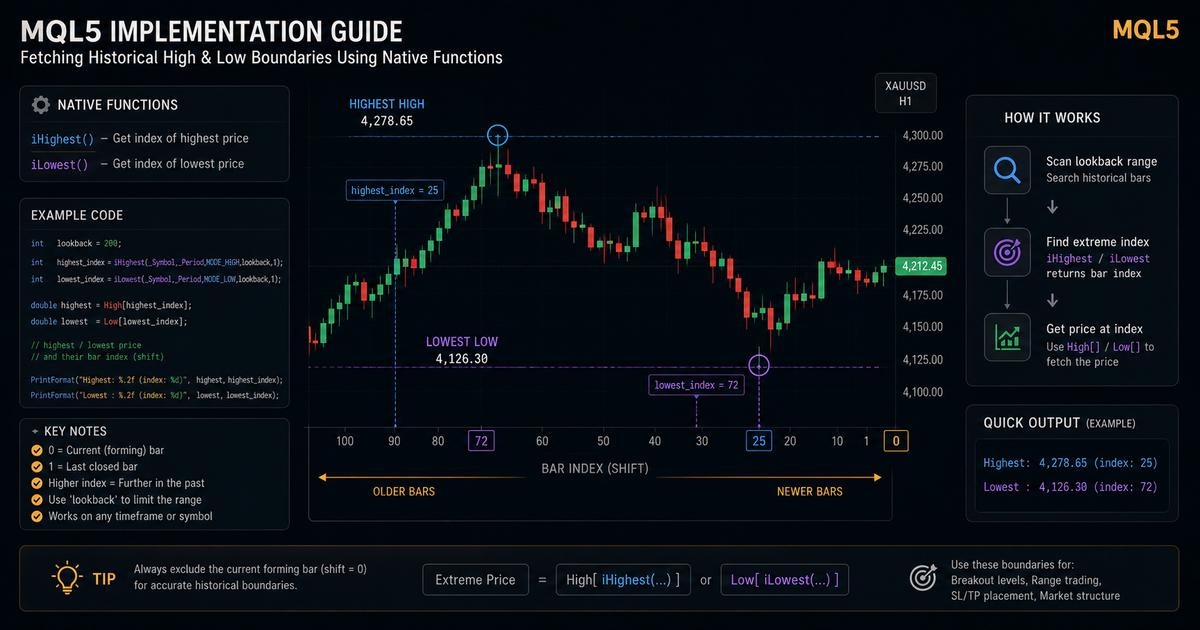

The most prevalent logical flaw when transitioning to MQL5 is confusing index retrieval with absolute valuation. The iHighest and iLowest core functions do not return price values like 1.09200 or 4278.65. Instead, they calculate and return a Bar Index (Historical Offset) representing the relative positional location of the candle containing the extreme value within a specified scanning range.

For example, if your system scans a series of 20 historical bars and the absolute lowest price occurred exactly 5 hours ago, the function passes the integer value 5 back into your application thread. The developer must then pass this index parameter into separate price array methods to isolate the physical quotation.

Function Syntax Breakdown

The function signatures for native MQL5 array mapping require five specific inputs to isolate data accurately:

int iHighest(

string symbol, // Asset Symbol (e.g., _Symbol or "XAUUSD")

ENUM_TIMEFRAMES timeframe, // Timeframe matrix (e.g., PERIOD_CURRENT, PERIOD_H1)

ENUM_SERIES_INFO_INTEGER type, // Search Mode property (MODE_HIGH or MODE_LOW)

int count=WHOLE_ARRAY,// Data depth to search (Total bars array)

int start=0 // Starting bar offset (0 maps live forming tick)

);Practical Deployment: Dynamic Structural Stop-Loss Engine

To complement our structural foundational framework detailed in Building a Trend-Following Algorithm: Multi-Timeframe EMA Filters in MQL5, your system must calculate invalidation boundaries dynamically based on low-timeframe wick parameters. The production-ready solution below can be integrated seamlessly into your existing trade logic layers:

//+------------------------------------------------------------------+

//| Computes Dynamic Protective Stop-Loss Based on Low-Timeframe Lows|

//+------------------------------------------------------------------+

double CalculateStructuralStopLoss(int lookbackBars)

{

// 1. Fetch the Bar Index of the absolute lowest wick (offset by 1 to isolate closed structural bars)

int targetLowIndex = iLowest(_Symbol, PERIOD_CURRENT, MODE_LOW, lookbackBars, 1);

if(targetLowIndex != -1)

{

// 2. Pass the index integer to query the historical price array structure

double absoluteLowPrice = iLow(_Symbol, PERIOD_CURRENT, targetLowIndex);

return absoluteLowPrice;

}

return 0.0; // Fail-Safe trigger to reject trade placement if historical data is uninitialized

}

When your H1 trend filter establishes a persistent bullish bias state, and your lower M1/M5 chart triggers a execution pattern, calling CalculateStructuralStopLoss(15); maps the lowest local structural boundary within the past 15 bars, creating a mathematically defensible risk wall against systemic noise.

Algorithmic Safeguards (MQL5 Development Gotchas)

- Data Out-of-Range Handling: If the local Terminal has not fully cached the asset's historical chart data from the broker server, the function will return -1. Your logic must explicitly reject transaction processing on a -1 output to avoid execution failures.

- Timeframe Asynchronicity: When executing cross-timeframe structures (e.g., querying H4 data boundaries from an M5 script), make sure you use an initial validation function in

OnInit()to check if the high-timeframe series is synced with live server times. - Intra-Bar Shift Factors: Setting the

startindex parameter to0includes the unclosed, real-time fluctuating candle. For stable structural calculations, setting the value to1ensures your system acts only on finalized, non-repainting datasets.

Strategic Optimization Matrix

By combining native high-low queries with localized risk modules, algorithms can automate precise trade setups across any liquid distribution asset class:

| Target Application | Function Setup | Lookback Scope | Execution Benefit |

|---|---|---|---|

| Breakout Entry Trigger | iHighest(..., MODE_HIGH, count, 1) | 20 - 50 Bars | Mitigates premature false breakout orders |

| Long Stop-Loss Placement | iLowest(..., MODE_LOW, count, 1) | 10 - 25 Bars | Positions hard stops outside local liquidity sweeps |

| Dynamic Range Expansion | Both Functions Combined | 100+ Bars | Enables quantitative volatility-based scale tracking |

Conclusion: Building Scalable Systems

Mastering the programmatic use of iHighest and iLowest allows you to shift from complex, slow manual loop routines to optimized, native C-style architecture. This procedural upgrade ensures your algorithmic execution calculations occur within milliseconds—preserving execution efficiency and locking in edge parameters before retail noise expands.

Quantitative Development FAQ

Do iHighest and iLowest functions in MQL5 directly return absolute price levels?

No, both functions return the bar index (historical offset) where the highest or lowest value was located within the designated range. To extract the actual price, you must pass this returned index into iHigh() or iLow() functions, or fetch it via a pre-synchronized MqlRates structure array.

Why does MQL5 require a different structural paradigm for iHighest compared to MQL4?

MQL4 allowed immediate global pointer referencing, whereas MQL5 utilizes an asynchronous event-driven architecture. Developers must specify distinct series enumeration fields (such as MODE_HIGH or MODE_LOW) and ensure underlying historical data buffers are synchronized to prevent runtime out-of-range critical errors.